Health insurance in Nigeria remains a critical component of the country’s healthcare system, yet its reach and effectiveness are still limited. Despite the establishment of frameworks such as the National Health Insurance Scheme (NHIS) and the broader National Health Insurance Plan, a large proportion of Nigerians continue to rely on out-of-pocket payments for healthcare. This exposes millions of households to financial risk and often leads to delayed or avoided treatment.

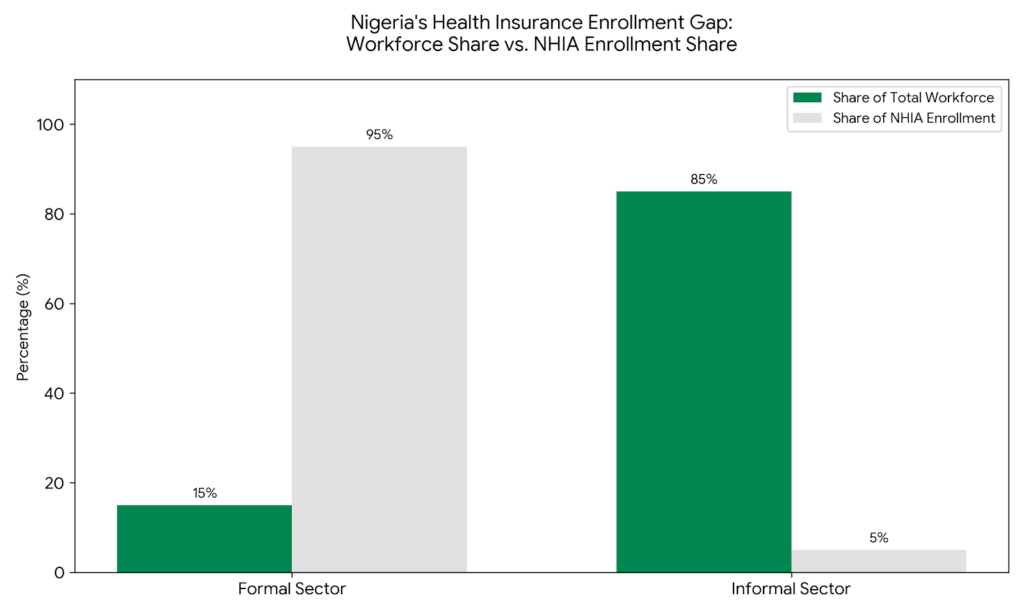

Data show that fewer than 5% of Nigerians are enrolled in the NHIS, while approximately 70% of healthcare spending is financed directly by individuals. This highlights a significant gap between policy intentions and real-world outcomes. While efforts by the Federal Ministry of Health and other stakeholders aim to improve coverage, structural, economic, and social barriers continue to limit progress.

Understanding the state of health insurance in Nigeria requires examining not only the systems in place but also the challenges affecting implementation and the opportunities for reform. This article explores these dimensions, providing a comprehensive view of where Nigeria stands and what lies ahead.

Understanding the Structure of Health Insurance in Nigeria

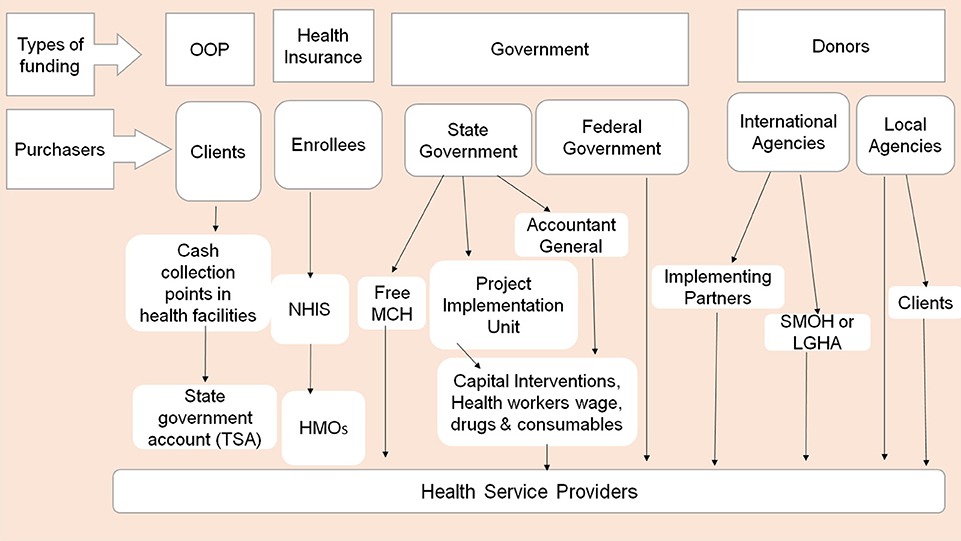

Nigeria’s health insurance system is built on national frameworks designed to improve access to affordable healthcare. These structures involve multiple stakeholders, including government institutions, healthcare providers, and insurance administrators, all working toward the goal of universal health coverage.

Overview of the National Health Insurance Scheme (NHIS)

The National Health Insurance Scheme (NHIS), launched in 2005, was created to provide financial protection against the high cost of healthcare. Its primary objective is to ensure that Nigerians can access essential health services without experiencing financial hardship.

However, despite its long-standing presence, NHIS has struggled to achieve widespread coverage. Enrollment remains low, and the scheme has largely benefited those in formal employment, leaving the majority of the population, particularly in the informal sector, uncovered.

Role of the Federal Ministry of Health in Health Insurance

The Federal Ministry of Health plays a central role in shaping policies and overseeing the implementation of health insurance initiatives. It is responsible for setting national health priorities, coordinating programs, and ensuring alignment with broader goals such as universal health coverage.

However, challenges such as fragmented governance and weak coordination have historically limited the effectiveness of health policies in Nigeria.

The National Health Insurance Plan and Its Objectives

The National Health Insurance Plan builds on the NHIS framework with a broader goal of expanding coverage and improving service delivery. It aims to address gaps in access, enhance quality, and ensure that healthcare services are affordable for all Nigerians.

Despite these ambitions, achieving universal coverage remains a work in progress, requiring sustained policy reform and system strengthening.

Current State of Health Insurance in Nigeria

The current state of health insurance in Nigeria reflects a system with strong policy intentions but limited reach. While frameworks exist, their implementation has not yet translated into widespread access.

Coverage Levels and Enrollment Trends

National Health Insurance Registration remains low relative to Nigeria’s population. Most enrollees are in the formal sector, where participation is easier to enforce. Meanwhile, the informal sector, which accounts for a significant portion of the workforce, remains largely excluded.

This imbalance contributes to the overall low coverage rate and highlights the need for more inclusive models.

Access and Utilisation of Health Insurance Services

Access to healthcare services is uneven across Nigeria. Urban areas tend to have better infrastructure and service availability, while rural communities face significant barriers.

In addition, even among those enrolled in insurance schemes, issues such as limited service coverage and inconsistent quality can affect utilisation.

Public Awareness and Perception

Low awareness remains a major barrier to uptake. Many Nigerians are either unaware of health insurance options or do not fully understand how they work.

Trust also plays a significant role. Concerns about service quality and experiences with healthcare providers can influence decisions to enrol or remain in the system.

Key Challenges Affecting Health Insurance in Nigeria

The challenges facing health insurance in Nigeria are multifaceted, spanning economic, structural, and social dimensions. Addressing these challenges is essential for improving coverage and system effectiveness.

Low Awareness and Information Gaps

Studies show that limited awareness and understanding of health insurance contribute significantly to low enrollment rates. Without clear information, many individuals are unable to make informed decisions about participation.

Affordability and Income Constraints

For many Nigerians, especially those in the informal sector, irregular income makes it difficult to commit to regular premium payments. This limits participation even when the benefits of health insurance are recognised.

Trust and Service Delivery Issues

Service delivery challenges, including inefficiencies, poor infrastructure, and inconsistent quality of care, undermine trust in the system. Research highlights inadequate healthcare facilities and poor resource management as key barriers.

Structural and Policy Implementation Gaps

Despite existing policies, implementation remains inconsistent. Factors such as weak administrative capacity, poor coordination, and a lack of enforcement contribute to system inefficiencies.

Opportunities to Strengthen Health Insurance in Nigeria

While challenges persist, there are significant opportunities to improve health insurance in Nigeria and expand access to care.

Expanding Coverage Through Informal Sector Inclusion

The informal sector represents the largest opportunity for growth. Developing flexible and affordable insurance models tailored to this group can significantly increase coverage.

Leveraging Awareness and Advocacy

Targeted awareness campaigns can help bridge information gaps and improve trust. Community-based engagement, including youth-led advocacy, can play a critical role in increasing understanding and participation.

Strengthening Policy Implementation and Coordination

Improving coordination among stakeholders and ensuring consistent policy implementation can enhance system performance. Strong governance and accountability are key to achieving this.

Role of Data and Community Insights

Data-driven approaches can help identify barriers and inform targeted interventions. Understanding community-level realities is essential for designing effective solutions.

The Role of Community Engagement in Expanding Health Insurance Uptake

While policy frameworks are important, meaningful progress requires engagement at the community level. Systems alone cannot drive change without the participation and trust of the people they are designed to serve.

Why Community-Level Engagement Matters

Community engagement helps bridge the gap between policy and practice. It ensures that information is communicated in an accessible, relevant way, building trust and encouraging participation.

Youth as Drivers of Health Insurance Awareness

Young people play a key role in driving awareness and influencing behaviour within communities. Through peer engagement and advocacy, they can help simplify complex health insurance concepts and promote understanding.

Example of Community-Driven Approaches

Community-driven initiatives demonstrate how localised engagement can improve outcomes. Programs such as NSSF’s WeNaija platform highlight how youth-led advocacy can increase awareness, gather insights, and support improved health insurance uptake at the grassroots level.

The Future of Health Insurance in Nigeria

The future of health insurance in Nigeria depends on the ability to address systemic challenges while leveraging opportunities for reform. With strategic investments, stronger policy implementation, and increased community engagement, it is possible to expand coverage and improve access to care.

Nigeria’s healthcare system also presents opportunities for innovation, investment, and reform, particularly in areas such as digital health and public-private partnerships. By aligning these opportunities with effective policy frameworks, the country can move closer to achieving universal health coverage.

Conclusion

Health insurance in Nigeria remains a critical pathway to achieving equitable access to healthcare. While significant challenges persist, the opportunities for improvement are substantial.

By addressing awareness gaps, strengthening system efficiency, and fostering community engagement, Nigeria can expand coverage and reduce the financial burden of healthcare on its population. Achieving this will require coordinated action, sustained commitment, and a focus on inclusive solutions that leave no one behind.